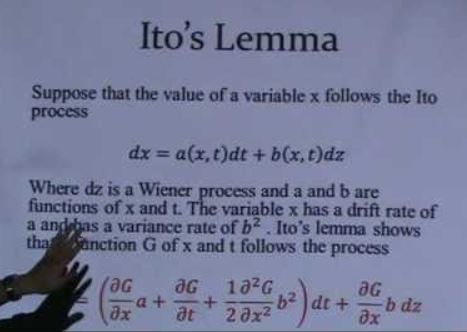

Stochastic calculus is the heart of quantitative finance, thanks to the Itô's lemma. Itô's lemma best known application is in the derivation of the Black–Scholes equation for option pricing.

• A class given by a one of my teacher a long time ago in university (French): Here.

A stochastic process St is said to follow a Geometric Brownian motion (GBM) if it satisfies the following stochastic differential equation (SDE):

(using MathML / MathAjax)

For example the GBM is used in the Monte Carlo famous stock price simulation. In regard to simulating stock prices, the most common model is geometric Brownian motion (GBM). GBM assumes that a constant drift is accompanied by random shocks. While the period returns under GBM are normally distributed, the consequent multi-period price levels are lognormally distributed.

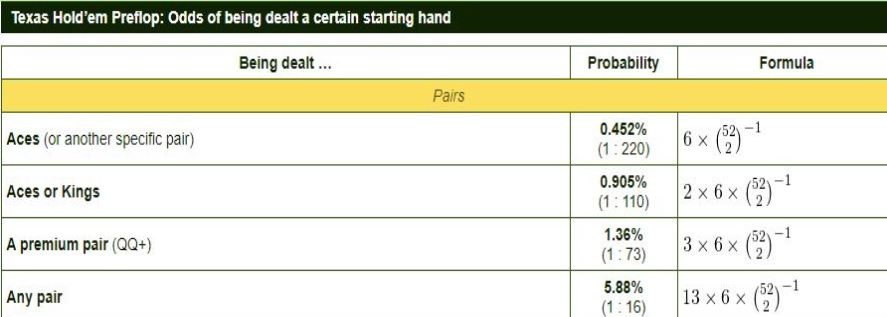

Combination and binomial coefficient are the basic for many interesting easy calculations, as probability of winning the EuroMillions or having a Ace pair in Texas Holdem poker.

• The main combination formula for the k combinations over n elements. C is noted as the binomial coefficient:

In order to win the big first prize in the EuroMillions you should get the 5 correct numbers between 1 to 50 and the 2 correct star numbers between 1 to 11.

This results in 116'531'800 possibilities. So by playing only one grid / game you have only 0.0000000085814% of winning the big prize (1/116'531'800).

Example of probabilities of having a nice pair in Texas Holder poker :) 🤠: